Home Loans for Self Employed & 1099 Borrowers

No W2s | No Tax Returns | Flexible Requirements

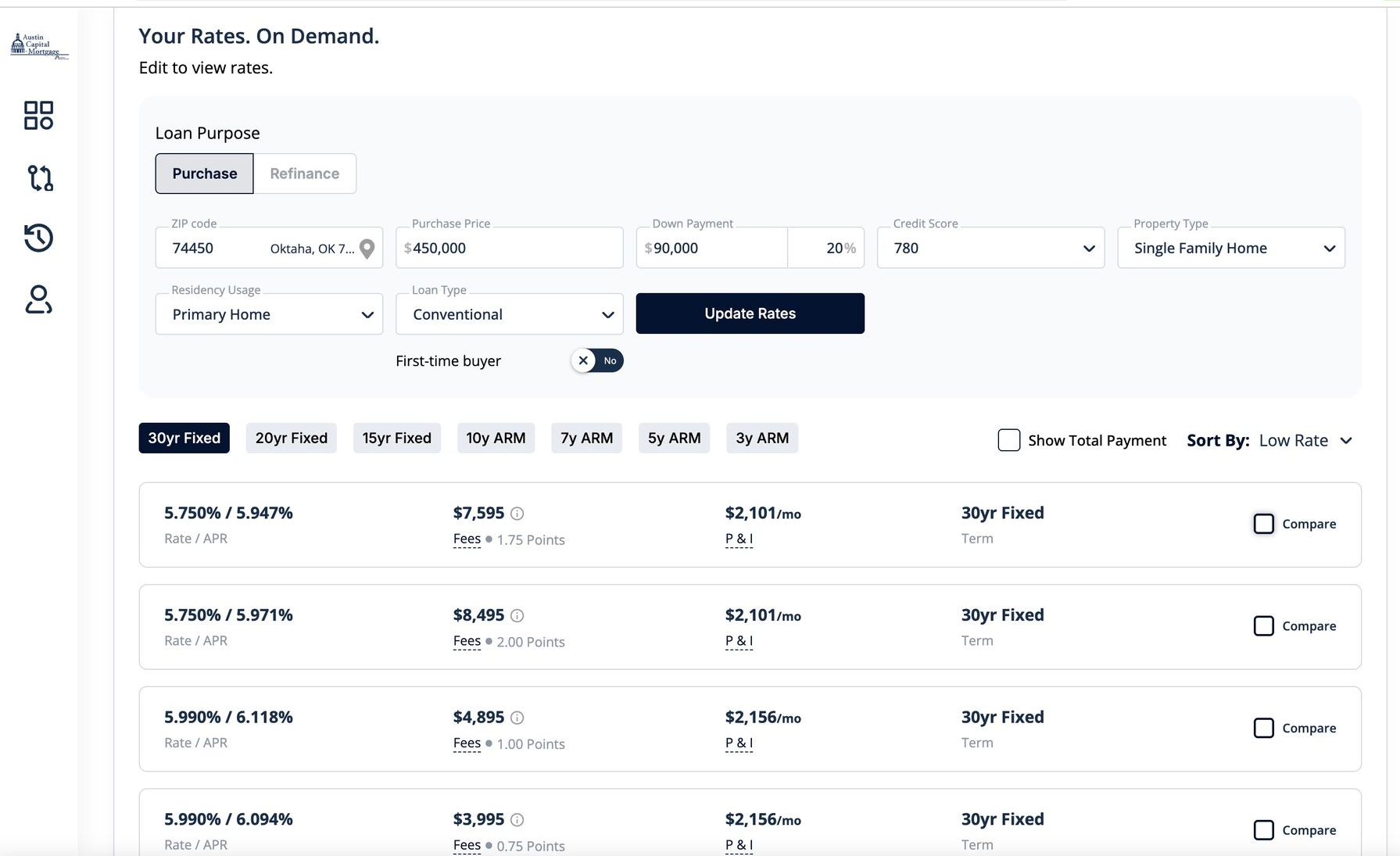

We compare 100+ lenders to find you the best mortgage rates.

- 1 Day Pre Approval

- In-house Underwriting

- Faster Closings (7-21 days)

Self Employed? Get Pre Approved in a Day!

It only takes 2 minutes, and won't affect your credit score.

Recently Funded Homes

From denied applications to signed contracts, here’s what we’ve funded lately.

Why Choose Us?

Our Process

Our mortgage process is designed to help you see the best loan options you actually qualify for before you commit to a full application.

Individual File Review

Each loan file is reviewed on a case-by-case basis before lender options are presented.

One Day Pre-Approval

Get Pre-Approved in 24 hours. Available for complete files.

Access to Multiple Lenders

We shop 100+ lenders to identify the best loan options for your scenario.

100% Online Application, 5 Star Client Experience

Our average client rating is 5 stars, thanks to our streamlined online process and fast closings.

Client Reviews: 5 Star Avg. User Rating

Austin Capital Mortgage is the highest rated mortgage lender in Texas.

Our average user customer rating is 5 stars. Here's what our clients say.

What are the eligibility requirements for self employed loans in 2025?

You’ll still need to meet the minimum mortgage requirements that apply to all borrowers, but lenders will scrutinize your finances more closely.

Guidelines vary from lender to lender, but the factors often used to determine the financial health and viability of your business include:

→ How the business operates

Lenders want to ensure that your business is financially sound.

An underwriter may research the location and type of business you’re in, how much demand there is for your product and how likely your business is to stay financially strong and profitable.

→ Personal income vs. business income

If you’re using income from your business to qualify for a loan, your lender may want to see evidence that your business has a healthy cash flow and isn’t buried in debt.

Personal income is typically verified with individual tax returns.

→ Your income stability

A lender may consider you to be at higher risk of missing mortgage payments if your earnings tend to vary from month to month.

That’s why some lenders ask for additional proof that your business is stable and that you have enough cash flow to handle a lower-earning month.

→ How long you’ve been self-employed

A lender prefers for you to have at least two years of experience earning income from self-employment.

The approval process may be simpler, however, if you’ve been in business for at least five years.

What forms/documents do I need for a self employed home loan?

For self-employed people looking for a mortgage, lenders typically request documents that provide a clear picture of your income stability and business viability.

- Personal Tax Returns

Your two most recent tax returns help demonstrate steady self-employment earnings.

However, some lenders may be satisfied with just last year’s tax return if you’ve been self-employed for at least a year.

- Profit and Loss Statements

Also called a P&L for short, this financial statement shows how much total profit you’ve made after subtracting your business expenses.

Lenders expect these documents to show earnings similar to or higher than what you listed as income on your tax returns.

- CPA Letters

Lenders may ask your certified public accountant (CPA) for a letter of explanation to verify your self-employment status.

- Documentation of Business Funds used for a Down Payment

If you want to use cash that’s in your business accounts to fund the down payment on a home, be prepared to provide extra documentation.

You may need business bank statements and tax returns, as well as a letter from your CPA or tax lawyer confirming that taking the funds won’t harm the business.

- IRS Transcripts

You may be asked to sign a form (IRS Form 4506-T) authorizing your lender to obtain a transcript of your tax return.

They’ll typically use it to verify that the information you provided in your loan application matches what’s in the IRS database.

- Business Tax Returns

The business tax returns you need to gather will depend on how your business is structured.

Here’s a breakdown of which forms you’ll likely need, depending on the type of business you operate.

FHA Home Loan for the Self Employed

Who is it for? First-time homebuyers and self-employed individuals with less-than-perfect credit or non-traditional income.

Credit Score Requirement

- 3.5% down payment:

580 or higher

- 10% down payment:

500-579

Down Payment Requirement

- As low as

3.5%.

- Pros:

Lower down payment requirements, more lenient credit and income requirements.

- Cons:

Mortgage insurance premiums (MIP) required, loan limits apply.

Conventional Home Loan for the Self Employed

Who is it for?

Self-employed individuals with strong credit and financial history.

Credit Score Requirement

- Typically 620 or higher.

Down Payment Requirement

- Usually

3% to 20%

of the purchase price.

- Pros:

Competitive interest rates, flexibility in loan terms.

- Cons:

Strict documentation requirements, higher credit score needed.

Bank Statement Loan for the Self Employed

Who is it for?

Self-employed borrowers looking for an alternative income verification.

Credit Score Requirement

- Varies by lender, but typically

620

or higher.

Down Payment Requirement

- Varies by lender.

- Pros:

Uses bank statements for income verification, helpful for self-employed with fluctuating income.

- Cons:

Higher interest rates, may require larger down payment.

Non QM Loans for Self Employed Borrowers

Who is it for?

Borrowers who don't meet traditional mortgage standards, including self-employed individuals with complex income.

Credit Score Requirement

- Varies widely among lenders, but

620

or higher is common.

Down Payment Requirement

- Varies by lender.

- Pros:

Flexible eligibility criteria, considers non-traditional income.

- Cons:

Higher interest rates, shorter loan terms.

VA Home Loan for the Self Employed

Who is it for?

Eligible veterans and active-duty service members, including self-employed individuals.

Credit Score Requirement

- No

set

minimum, but most lenders prefer

620

or higher.

Down Payment Requirement

- No down payment required for most borrowers.

- Pros:

No down payment required, competitive interest rates.

- Cons: Limited to eligible veterans and active-duty service members, VA funding fee.

USDA Home Loan

Who is it for?

Eligible rural borrowers, including some self-employed individuals.

Credit Score Requirement

- Typically

640

or higher.

Down Payment Requirement

- No down payment

required.

- Pros:

No down payment required, low-interest rates.

- Cons:

Limited to eligible rural borrowers, income limits apply.

Frequently Asked Questions

Here are some of the most common questions we get, with a quick way to connect with our mortgage advisors for more detailed answers.

NMLS # 1955132

Have questions or feedback?

Reach out to our support team at:

Or give us a call at:

2023 Austin Capital Mortgage, a division of Aspire Home Loan | All Rights Reserved | Member FDIC | NMLS 1955132 | Privacy Policy